When it comes to securing a home loan, choosing the right financial institution can make all the difference. Credit unions have emerged as a popular alternative to traditional banks, offering personalized service and competitive rates. But are credit unions good for home loans? This question has gained traction among homebuyers seeking affordable and flexible mortgage solutions. Credit unions, as member-focused organizations, often prioritize the needs of their members over profits, making them an attractive option for those navigating the home-buying process.

For many prospective homeowners, the appeal of credit unions lies in their unique structure and values. Unlike banks, credit unions are not-for-profit entities owned by their members, which means they often pass on savings in the form of lower interest rates and reduced fees. This member-centric approach can translate into significant savings over the life of a mortgage. Additionally, credit unions are known for their personalized customer service, which can simplify the often-complex process of securing a home loan. Whether you're a first-time buyer or looking to refinance, understanding how credit unions operate can help you make an informed decision.

However, while credit unions offer many advantages, they may not be the perfect fit for everyone. Factors such as membership eligibility, loan product availability, and branch accessibility can influence whether a credit union is the right choice for your home loan needs. As we delve deeper into this topic, we’ll explore the benefits and potential drawbacks of credit unions, compare them to traditional banks, and provide actionable insights to help you determine if a credit union is the best option for your home financing journey.

Read also:

Table of Contents

- What Are Credit Unions and How Do They Differ From Banks?

- Are Credit Unions Good for Home Loans? What Are the Benefits?

- How Do Credit Union Mortgage Rates Compare to Banks?

- What Are the Potential Drawbacks of Using a Credit Union for Home Loans?

- How to Qualify for a Home Loan at a Credit Union?

- Can Credit Unions Offer Special Programs for First-Time Homebuyers?

- What Should You Consider Before Choosing a Credit Union for Your Home Loan?

- FAQs About Credit Unions and Home Loans

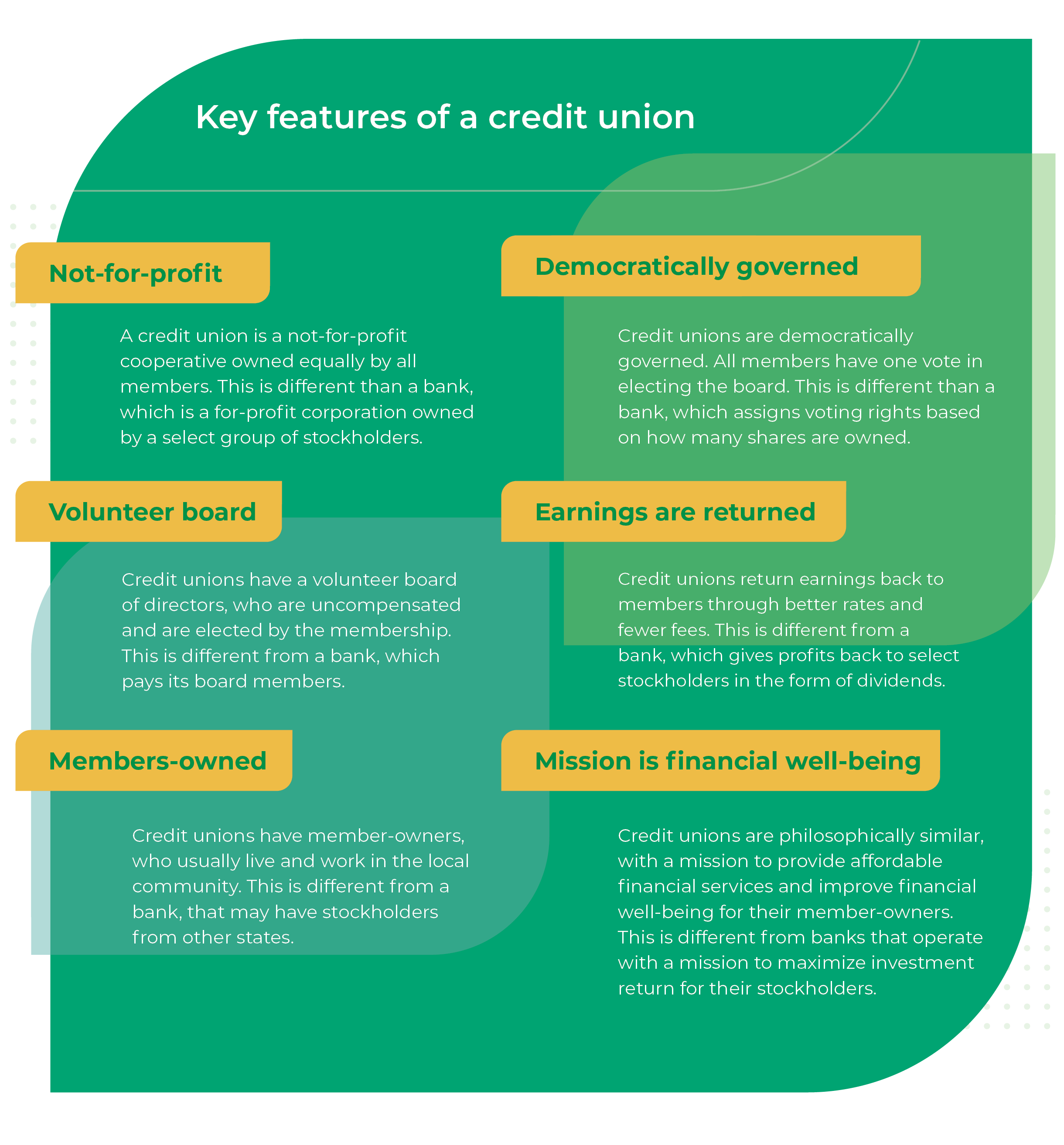

What Are Credit Unions and How Do They Differ From Banks?

Credit unions are member-owned financial cooperatives that provide a wide range of banking services, including savings accounts, loans, and mortgages. Unlike traditional banks, which are profit-driven corporations, credit unions operate as not-for-profit organizations. This fundamental difference shapes how credit unions approach lending and customer service. For example, credit unions often reinvest their earnings back into the organization to benefit their members, rather than distributing profits to shareholders.

Key Differences Between Credit Unions and Banks

One of the most significant distinctions between credit unions and banks is their ownership structure. Banks are owned by shareholders, while credit unions are owned by their members. This means that credit union members have a say in how the institution is run, including voting on board members and key decisions. Additionally, credit unions typically offer lower fees and better interest rates because they are not focused on generating profits for external investors.

Membership Eligibility

Another critical difference is membership eligibility. To join a credit union, you must meet specific criteria, such as living in a particular area, working for a certain employer, or belonging to a specific organization. While this requirement can limit access, many credit unions have expanded their membership criteria to include a broader range of individuals.

Are Credit Unions Good for Home Loans? What Are the Benefits?

Credit unions offer several advantages when it comes to home loans, making them a compelling choice for many borrowers. One of the most significant benefits is the potential for lower interest rates. Because credit unions are not-for-profit, they can often offer more competitive rates compared to traditional banks. This can result in substantial savings over the life of a mortgage, especially for long-term loans.

Personalized Customer Service

In addition to competitive rates, credit unions are renowned for their personalized customer service. Unlike large banks, where customers may feel like just another account number, credit unions often provide a more hands-on approach. Loan officers at credit unions are typically more accessible and willing to work with borrowers to find solutions that meet their unique needs. This personalized service can be particularly beneficial for first-time homebuyers or those with less-than-perfect credit.

Flexible Loan Options

Credit unions also tend to offer more flexible loan options. For example, they may provide adjustable-rate mortgages (ARMs), fixed-rate mortgages, and even specialized programs for low-income borrowers. Some credit unions even offer portfolio loans, which are held in-house rather than sold to investors, allowing for more lenient qualification requirements.

Read also:Discover The World Of 7starmovies Hd Your Gateway To Highquality Entertainment

How Do Credit Union Mortgage Rates Compare to Banks?

When comparing mortgage rates, credit unions often come out ahead of traditional banks. According to industry data, credit unions typically offer interest rates that are 0.25% to 0.50% lower than those of banks. This difference may seem small, but it can translate into thousands of dollars in savings over the life of a loan. For example, on a 30-year mortgage of $300,000, a 0.25% reduction in interest could save you over $10,000.

Why Credit Unions Can Offer Lower Rates

The lower rates offered by credit unions are largely due to their not-for-profit status. Since they don’t have to generate profits for shareholders, credit unions can pass on savings to their members. Additionally, credit unions often have lower overhead costs compared to large banks, allowing them to offer more competitive rates. This cost advantage is particularly beneficial for borrowers seeking affordable home financing options.

Comparing Closing Costs

Beyond interest rates, credit unions also tend to have lower closing costs. These costs, which include fees for appraisals, title insurance, and loan origination, can add up quickly. By choosing a credit union, borrowers may save hundreds or even thousands of dollars in upfront expenses, making homeownership more accessible.

What Are the Potential Drawbacks of Using a Credit Union for Home Loans?

While credit unions offer many advantages, they are not without their limitations. One potential drawback is membership eligibility. As mentioned earlier, credit unions often require members to meet specific criteria, which can exclude some borrowers. Additionally, credit unions may have fewer branches and ATMs compared to large banks, which could be inconvenient for borrowers who value accessibility.

Limited Loan Product Availability

Another downside is the limited availability of loan products. Credit unions may not offer the same variety of mortgage options as larger banks, particularly when it comes to specialized loans like jumbo mortgages or government-backed loans. This limitation could be a dealbreaker for borrowers with unique financing needs.

Slower Adoption of Technology

Finally, credit unions sometimes lag behind banks in terms of technology. While many credit unions have modernized their online banking platforms, some still rely on outdated systems that may not offer the same level of convenience as larger banks. Borrowers who prioritize digital tools and mobile apps may find this aspect less appealing.

How to Qualify for a Home Loan at a Credit Union?

Qualifying for a home loan at a credit union is similar to the process at a traditional bank, but there are a few key differences to keep in mind. The first step is to become a member of the credit union, which typically involves meeting eligibility requirements and paying a small membership fee. Once you’re a member, you can apply for a mortgage by providing documentation such as proof of income, tax returns, and bank statements.

What Credit Unions Look For

Credit unions generally look for borrowers with stable income, a good credit score, and a manageable debt-to-income ratio. However, they may be more flexible than banks when it comes to credit scores and other qualifications. This flexibility can make credit unions an excellent option for borrowers who may not meet the strict requirements of traditional lenders.

Tips for a Smooth Application Process

To ensure a smooth application process, consider the following tips:

- Gather all necessary documentation before applying.

- Review your credit report and address any errors.

- Work with a loan officer to understand your options.

Can Credit Unions Offer Special Programs for First-Time Homebuyers?

Yes, many credit unions offer specialized programs for first-time homebuyers, making homeownership more accessible. These programs often include reduced down payment requirements, lower interest rates, and educational resources to help buyers navigate the process. For example, some credit unions partner with government agencies to offer FHA or USDA loans, which are designed to assist low- to moderate-income borrowers.

Advantages of Credit Union Programs

Credit union programs for first-time homebuyers often come with additional perks, such as free financial counseling and workshops. These resources can be invaluable for buyers who are unfamiliar with the mortgage process or need help improving their financial literacy.

Examples of Credit Union Initiatives

For instance, Navy Federal Credit Union offers a “HomeBuyers Choice” program that allows borrowers to finance up to 100% of the home’s value. Similarly, PenFed Credit Union provides a “First-Time Homebuyer Program” with competitive rates and flexible terms.

What Should You Consider Before Choosing a Credit Union for Your Home Loan?

Before committing to a credit union for your home loan, it’s essential to weigh the pros and cons. Consider factors such as membership eligibility, loan product availability, and the credit union’s reputation. Additionally, evaluate the level of customer service and the convenience of their branch and ATM network. By carefully assessing these elements, you can determine whether a credit union aligns with your financial goals and needs.

Questions to Ask Yourself

- Do I meet the credit union’s membership requirements?

- Does the credit union offer the type of loan I need?

- How accessible are their branches and ATMs?

Final Thoughts

Ultimately, the decision to choose a credit union for your home loan depends on your individual circumstances and priorities. By conducting thorough research and comparing your options, you can make an informed choice that sets you on the path to successful homeownership.

FAQs About Credit Unions and Home Loans

Are credit unions good for home loans?

Yes, credit unions are often a great choice for home loans due to their competitive rates, personalized service, and flexible terms. However, it’s important to consider factors like membership eligibility and loan product availability before making a decision.

What are the main advantages of using a credit union for a mortgage?

Credit unions offer lower interest rates, reduced fees, and personalized customer service. They also tend to have more flexible qualification requirements, making them an excellent option for many borrowers.

How do I find a credit union that offers home loans?

To find a credit union that offers home loans, start by researching local options and checking their membership requirements. You can also visit the National Credit Union Administration (NCUA) website for a list of federally insured credit unions.

Conclusion

Choosing the right financial institution for your home loan is a critical decision that can impact your financial future. Credit unions, with their member-focused approach and competitive offerings, are worth considering for anyone in the market for a mortgage. By understanding the benefits and potential drawbacks, you can determine if a credit union is the right fit for your home financing needs. Whether you’re a first-time buyer or looking to refinance, credit unions provide a compelling alternative to traditional banks.

For more information on credit unions and their services, visit the