Have you ever wondered how the Federal Reserve's interest rates impact your daily life and the broader economy? The Federal Reserve, often referred to as "the Fed," plays a pivotal role in shaping the U.S. economy through its monetary policy tools. One of the most critical tools at its disposal is the adjustment of interest rates. These rates influence everything from the cost of borrowing money to the overall health of financial markets. Whether you're a business owner, an investor, or simply someone trying to manage personal finances, understanding how federal reserve interest rates work is essential.

Interest rates set by the Federal Reserve affect not only the economy but also individual households. When the Fed raises or lowers interest rates, it sends ripples through various sectors, influencing mortgage rates, credit card interest, and even job creation. For instance, lower interest rates can stimulate spending and investment, while higher rates are often used to curb inflation. This delicate balancing act ensures economic stability, but it also requires constant monitoring and adjustment by policymakers. By the end of this article, you'll have a clearer understanding of how these rates are determined and their far-reaching effects.

Moreover, the Federal Reserve's decisions on interest rates are closely watched by economists, investors, and policymakers worldwide. These decisions don't just affect the U.S. economy; they can also influence global markets. For example, when the Fed raises interest rates, it can lead to a stronger U.S. dollar, affecting international trade and emerging markets. Conversely, a rate cut can weaken the dollar, making U.S. exports more competitive. This interconnectedness highlights why federal reserve interest rates are such a crucial topic for anyone interested in economics or finance. So, let's dive deeper into the mechanics, implications, and future outlook of these rates.

Read also:

Table of Contents

- What Are Federal Reserve Interest Rates?

- How Are Federal Reserve Interest Rates Determined?

- Why Do Federal Reserve Interest Rates Change?

- How Do Interest Rates Affect the Economy?

- What Happens When the Fed Raises Interest Rates?

- What Happens When the Fed Lowers Interest Rates?

- How Can You Prepare for Interest Rate Changes?

- The Future of Federal Reserve Interest Rates

What Are Federal Reserve Interest Rates?

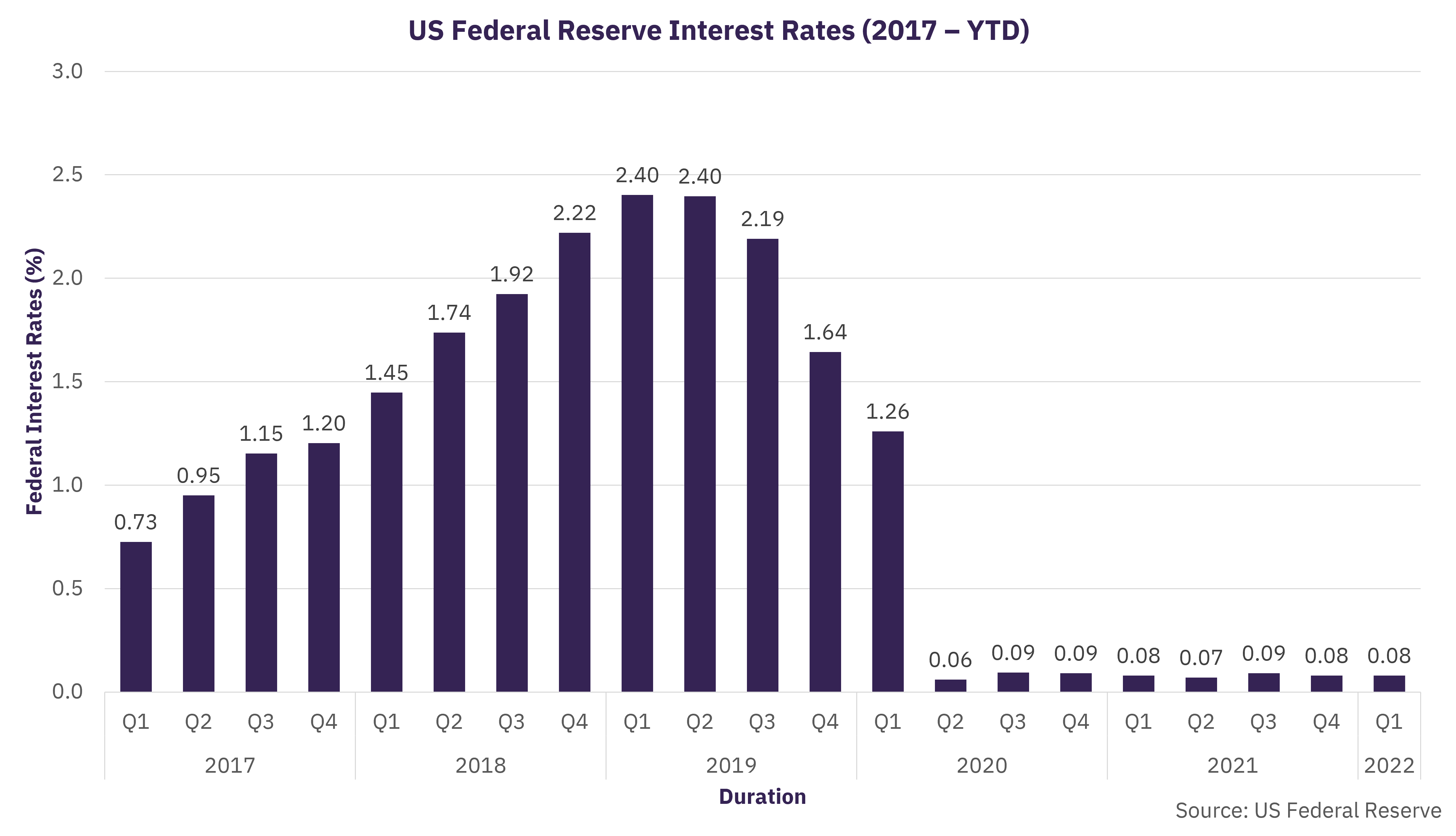

Federal Reserve interest rates refer to the benchmark rates that the Federal Reserve sets to influence the cost of borrowing and lending money within the economy. These rates are a cornerstone of monetary policy and are used to achieve specific economic goals, such as controlling inflation, promoting employment, and ensuring financial stability. The most well-known of these rates is the federal funds rate, which is the interest rate at which banks lend to each other overnight.

But why are these rates so important? Think of them as the heartbeat of the economy. When the Fed adjusts these rates, it influences everything from the interest you pay on your credit card to the returns you earn on your savings account. For example, when the federal funds rate is low, borrowing becomes cheaper, encouraging businesses to invest and consumers to spend. Conversely, when the rate is high, borrowing becomes more expensive, which can slow down economic activity and help control inflation.

Other key rates include the discount rate, which is the interest rate the Fed charges banks for borrowing directly from it, and the interest rate on reserve balances, which is the rate paid to banks for holding reserves at the Fed. These rates work together to shape the broader financial landscape, affecting everything from housing markets to stock prices. Understanding these mechanisms is crucial for anyone looking to navigate the complexities of the modern economy.

How Are Federal Reserve Interest Rates Determined?

The process of determining federal reserve interest rates is a meticulous one, involving a combination of economic data analysis, forecasting, and decision-making by the Federal Open Market Committee (FOMC). The FOMC, which consists of 12 members, meets eight times a year to assess the state of the economy and decide whether to adjust interest rates. These meetings are closely watched by economists, investors, and the general public, as their outcomes can significantly impact financial markets.

So, what factors influence these decisions? The FOMC considers a wide range of economic indicators, including inflation rates, employment levels, GDP growth, and global economic conditions. For instance, if inflation is rising faster than the Fed's target of 2%, the committee might decide to raise interest rates to cool down the economy. Similarly, if unemployment is high or economic growth is sluggish, the Fed might lower rates to stimulate borrowing and spending.

Another critical aspect of this process is the Fed's dual mandate: to promote maximum employment and stable prices. Balancing these two goals is no easy task, as policies that promote one might hinder the other. For example, lowering interest rates to boost employment can sometimes lead to higher inflation, while raising rates to control inflation might slow down job creation. This delicate balancing act requires careful consideration and a deep understanding of economic dynamics.

Read also:Exploring The Excitement Of Ridiculousness Season 19

Why Do Federal Reserve Interest Rates Change?

Changes in federal reserve interest rates are not arbitrary; they are driven by the Fed's efforts to achieve its economic objectives. One of the primary reasons for adjusting these rates is to manage inflation. When inflation is too high, the Fed raises interest rates to make borrowing more expensive, thereby reducing consumer spending and slowing down price increases. On the other hand, when inflation is too low, the Fed might lower rates to encourage spending and investment, helping to boost economic activity.

Another reason for rate changes is to influence employment levels. Lower interest rates can stimulate job creation by making it cheaper for businesses to borrow money and expand their operations. This, in turn, can lead to increased hiring and lower unemployment rates. Conversely, if the economy is overheating and inflation is becoming a concern, the Fed might raise rates to cool things down and prevent excessive job growth that could lead to wage inflation.

Global economic conditions also play a role in these decisions. For example, if there's a financial crisis in another part of the world, it can affect the U.S. economy by reducing demand for American goods and services. In such cases, the Fed might lower interest rates to support domestic economic growth. Similarly, geopolitical events, such as trade disputes or pandemics, can influence the Fed's decisions as they assess the potential impact on the U.S. economy.

How Do Interest Rates Affect the Economy?

Impact on Consumers

When the Federal Reserve adjusts interest rates, it has a direct impact on consumers. For instance, when interest rates are low, borrowing becomes more affordable, which can lead to increased spending on big-ticket items like homes, cars, and appliances. This is because lower rates translate to lower monthly payments on loans and mortgages, making it easier for consumers to take on debt. Additionally, credit card interest rates may also decrease, providing some relief to those carrying balances.

On the flip side, when interest rates rise, the cost of borrowing increases, which can discourage spending. Higher mortgage rates, for example, can make homeownership less accessible, while increased credit card rates can lead to higher monthly payments. This can put a strain on household budgets, especially for those who rely heavily on credit. However, higher rates can also benefit savers, as banks may offer better returns on savings accounts and certificates of deposit (CDs).

Impact on Businesses

Businesses are also significantly affected by changes in federal reserve interest rates. When rates are low, companies can borrow money at a lower cost, allowing them to invest in new projects, expand operations, and hire more employees. This can lead to increased economic activity and job creation, benefiting the broader economy. Lower rates can also improve business confidence, encouraging entrepreneurs to take risks and innovate.

Conversely, when interest rates rise, the cost of borrowing increases, which can dampen business investment. Companies may delay expansion plans or cut back on hiring, leading to slower economic growth. Higher rates can also impact stock prices, as investors may shift their focus from stocks to bonds, which offer higher returns in a rising rate environment. This can create volatility in financial markets, affecting businesses that rely on equity financing.

What Happens When the Fed Raises Interest Rates?

When the Federal Reserve raises interest rates, it's usually a signal that the economy is growing too quickly, and inflation is becoming a concern. Higher rates make borrowing more expensive, which can slow down consumer spending and business investment. For example, higher mortgage rates can reduce demand for homes, while increased loan rates can discourage businesses from taking on new projects. This, in turn, can help control inflation by reducing the amount of money circulating in the economy.

However, raising interest rates can also have negative side effects. For instance, it can lead to higher unemployment as businesses cut back on hiring or even lay off workers. It can also increase the cost of servicing existing debt, putting a strain on households and businesses that are already struggling. Additionally, higher rates can lead to a stronger U.S. dollar, which can hurt exporters by making American goods more expensive for foreign buyers.

Despite these challenges, raising interest rates is often necessary to maintain economic stability. By carefully managing the pace and magnitude of rate increases, the Fed can achieve a soft landing, where inflation is brought under control without causing a recession. This delicate balancing act requires constant monitoring and adjustment, as the Fed seeks to navigate the complexities of the modern economy.

What Happens When the Fed Lowers Interest Rates?

When the Federal Reserve lowers interest rates, it's typically a sign that the economy is slowing down, and the Fed wants to stimulate growth. Lower rates make borrowing cheaper, encouraging consumers to spend and businesses to invest. For example, lower mortgage rates can boost the housing market, while reduced loan rates can help businesses expand their operations. This can lead to increased economic activity, job creation, and higher consumer confidence.

However, lowering interest rates can also have downsides. For instance, it can lead to higher inflation if the economy overheats, as increased spending can drive up prices. It can also create asset bubbles, as investors chase higher returns in stocks and real estate, leading to unsustainable price increases. Additionally, lower rates can hurt savers, as banks may offer lower returns on savings accounts and CDs, reducing the income available to retirees and others who rely on interest payments.

Despite these risks, lowering interest rates is often necessary to support the economy during times of weakness. By making borrowing more affordable, the Fed can help businesses and consumers weather economic downturns and lay the groundwork for future growth. This proactive approach can help prevent recessions and ensure long-term economic stability.

How Can You Prepare for Interest Rate Changes?

With federal reserve interest rates constantly in flux, it's essential to be prepared for changes that could impact your financial situation. One way to do this is by paying attention to the Fed's announcements and understanding the economic indicators that influence their decisions. For example, keeping an eye on inflation rates, employment data, and GDP growth can give you a sense of whether rates are likely to rise or fall in the near future.

Another strategy is to adjust your financial plans based on the current interest rate environment. If rates are low, it might be a good time to take out a mortgage or refinance existing debt, as borrowing costs are lower. On the other hand, if rates are high, you might want to focus on paying down debt and building up your savings, as the returns on savings accounts and CDs may be more attractive. Additionally, diversifying your investments can help protect your portfolio from the volatility that often accompanies rate changes.

Finally, it's important to stay informed and seek professional advice if needed. Financial advisors can provide personalized guidance based on your specific circumstances, helping you navigate the complexities of interest rate changes. By taking a proactive approach, you can ensure that you're well-prepared for whatever the future holds.

The Future of Federal Reserve Interest Rates

As we look to the future, the trajectory of federal reserve interest rates will depend on a variety of factors, including economic growth, inflation, and global developments. While the Fed has signaled a commitment to maintaining price stability and promoting employment, the path forward is likely to be uncertain. For example, rising inflation pressures could lead to further rate hikes, while a slowdown in economic growth might prompt the Fed to lower rates.

Technological