Whether you're a first-time buyer or a seasoned homeowner looking to refinance, understanding the dynamics of current mortgage rates is crucial. Mortgage rates today are influenced by a myriad of factors, including economic conditions, inflation, and government policies. With the housing market constantly evolving, staying informed about mortgage rates today can help you make smarter financial decisions. The stakes are high—locking in a favorable rate can save you thousands of dollars over the life of your loan. As of late, mortgage rates today have shown fluctuations due to global economic uncertainties and shifts in monetary policy. For instance, the Federal Reserve's decisions on interest rates directly affect what lenders charge for home loans. If you're planning to buy a home soon, monitoring mortgage rates today can give you an edge. Not only will it help you time your purchase, but it will also allow you to compare offers from different lenders. With rates potentially rising or falling based on economic indicators, it's essential to act strategically. The good news is that understanding mortgage rates today doesn't have to be overwhelming. This guide will walk you through everything you need to know, from the factors influencing rates to strategies for securing the best deal. By the end, you'll have a clear roadmap to navigate the complexities of mortgage rates today and make informed decisions tailored to your financial goals. Let’s dive in and explore how you can take advantage of the current market conditions to achieve your homeownership dreams.

Table of Contents

- What Are Mortgage Rates Today and Why Do They Matter?

- How Are Mortgage Rates Today Determined?

- What Factors Influence Mortgage Rates Today?

- How Can You Lock in the Best Mortgage Rates Today?

- Is Now the Right Time to Buy with Mortgage Rates Today?

- What Are the Different Types of Mortgage Rates Today?

- How Do Mortgage Rates Today Affect Your Long-Term Financial Planning?

- Frequently Asked Questions About Mortgage Rates Today

What Are Mortgage Rates Today and Why Do They Matter?

Mortgage rates today are the interest rates that lenders charge borrowers for home loans. These rates are expressed as a percentage of the loan amount and play a pivotal role in determining the overall cost of homeownership. Whether you're purchasing a new home or refinancing an existing mortgage, the rate you secure will directly impact your monthly payments and the total interest you'll pay over the life of the loan. For example, even a small difference in mortgage rates today—say, 0.25%—can translate into thousands of dollars saved or spent over a 30-year mortgage term. Why do mortgage rates today matter so much? The answer lies in their ripple effect on your financial health. A lower mortgage rate means lower monthly payments, freeing up more of your income for other expenses or savings. On the flip side, higher rates can strain your budget, making it harder to afford the home you desire. Additionally, mortgage rates today influence the housing market as a whole. When rates are low, more people are incentivized to buy homes, driving up demand and potentially increasing home prices. Conversely, higher rates can cool down the market, making it a buyer's or seller's market depending on the circumstances. Understanding mortgage rates today is also crucial for timing your home purchase. Rates can fluctuate daily based on economic conditions, so keeping an eye on trends can help you decide when to lock in a rate. For instance, if you notice that mortgage rates today are trending downward, you might choose to wait a bit longer before committing. Conversely, if rates are on the rise, acting quickly could save you money in the long run. Ultimately, mortgage rates today are more than just numbers—they're a key factor in shaping your financial future.

How Are Mortgage Rates Today Determined?

Mortgage rates today are influenced by a complex interplay of factors, ranging from macroeconomic conditions to individual lender policies. One of the primary drivers is the state of the economy. When the economy is strong, with low unemployment and rising wages, lenders may increase mortgage rates today to manage demand. Conversely, during economic downturns, rates often decrease to encourage borrowing and stimulate growth. The Federal Reserve also plays a significant role by setting the federal funds rate, which indirectly impacts mortgage rates today. Although the Fed doesn't directly control mortgage rates, its decisions on interest rates can influence the broader financial markets. Another key factor is the bond market, particularly mortgage-backed securities (MBS). Lenders often sell home loans to investors in the form of MBS, and the yields on these securities are closely tied to mortgage rates today. When investor demand for MBS is high, rates tend to decrease. On the other hand, if investors seek higher returns elsewhere, such as in stocks, MBS yields may rise, pushing mortgage rates today higher. Inflation is another critical element. Lenders adjust mortgage rates today to account for inflation, as it erodes the purchasing power of money over time. Higher inflation typically leads to higher rates, while lower inflation can result in more favorable borrowing conditions.

Read also:

How Do Lenders Decide on Mortgage Rates Today?

Lenders also consider individual borrower factors when determining mortgage rates today. Your credit score, for instance, is a major determinant. Borrowers with higher credit scores are seen as less risky and are often offered lower rates. Similarly, the size of your down payment can influence the rate you're offered. A larger down payment reduces the lender's risk, potentially resulting in a better rate. Loan term and type also matter. Fixed-rate mortgages often have higher initial rates compared to adjustable-rate mortgages (ARMs), but they provide stability over time. Lenders also assess broader market conditions, such as housing demand and inventory levels, which can affect mortgage rates today.

What Role Do Government Policies Play?

Government policies can significantly impact mortgage rates today. Programs like those offered by the Federal Housing Administration (FHA) or the Department of Veterans Affairs (VA) provide loans with competitive rates, often benefiting first-time buyers and veterans. Additionally, federal initiatives to stimulate the housing market, such as lowering mortgage insurance premiums, can lead to more attractive rates. Understanding these influences can help you navigate the complexities of mortgage rates today and make informed decisions.

What Factors Influence Mortgage Rates Today?

Several interconnected factors influence mortgage rates today, and understanding them can help you better predict market trends. One of the most significant factors is inflation. When inflation rises, the purchasing power of money decreases, prompting lenders to increase mortgage rates today to compensate for the loss of value over time. For example, during periods of high inflation, you might notice mortgage rates today climbing, making borrowing more expensive. Conversely, low inflation often leads to lower rates, creating a more favorable environment for homebuyers. The bond market, particularly mortgage-backed securities (MBS), also plays a crucial role. Lenders bundle home loans into securities and sell them to investors. The demand for these securities affects mortgage rates today. When investor confidence is high, demand for MBS increases, driving rates down. However, if investors shift their focus to other assets, such as stocks, the demand for MBS may drop, causing mortgage rates today to rise. Additionally, global economic events, such as geopolitical tensions or international trade agreements, can impact investor sentiment and, by extension, mortgage rates today.

How Does Your Credit Score Affect Mortgage Rates Today?

Your credit score is a critical factor in determining the mortgage rates today that you qualify for. Lenders use credit scores to assess the risk of lending to you. Borrowers with higher scores—typically 740 or above—are considered low-risk and are often offered the most competitive rates. On the other hand, lower scores can result in higher mortgage rates today, as lenders seek to mitigate potential losses. Improving your credit score before applying for a mortgage can help you secure better rates and save money over the life of your loan.

Why Does Loan Type Matter for Mortgage Rates Today?

The type of loan you choose also influences mortgage rates today. Fixed-rate mortgages offer stability, with rates that remain constant throughout the loan term. However, they often come with higher initial rates compared to adjustable-rate mortgages (ARMs). ARMs typically start with lower rates but can increase after an introductory period, making them riskier in a rising-rate environment. Government-backed loans, such as FHA or VA loans, often have lower rates due to federal guarantees, making them an attractive option for eligible borrowers.

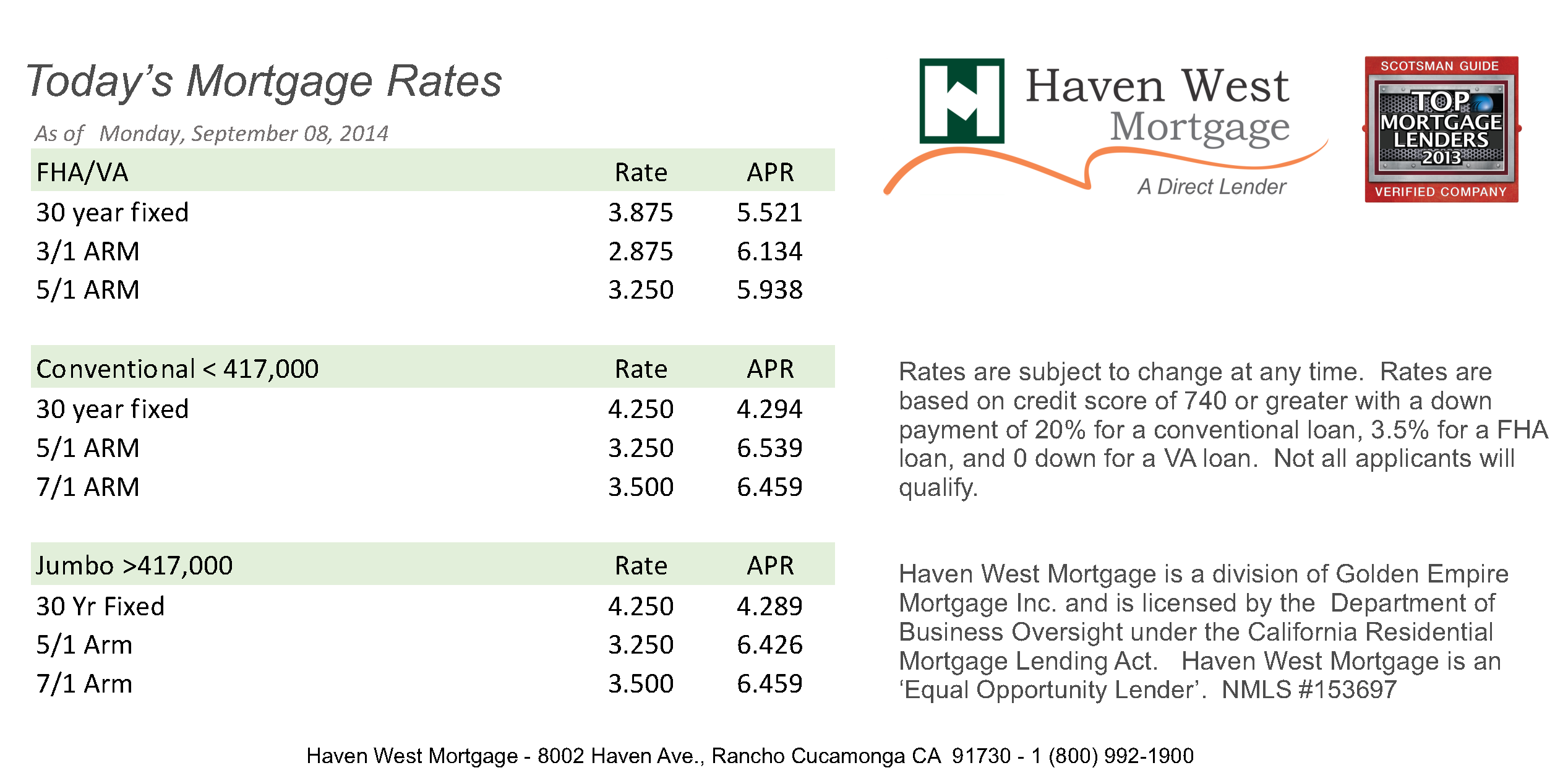

How Can You Lock in the Best Mortgage Rates Today?

Securing the best mortgage rates today requires a combination of preparation, timing, and strategic decision-making. One of the first steps is improving your financial profile. Lenders assess factors like your credit score, debt-to-income ratio, and employment history when determining mortgage rates today. By paying down existing debt, maintaining a stable income, and ensuring timely bill payments, you can position yourself as a low-risk borrower. A higher credit score, for instance, can unlock significantly lower rates, potentially saving you thousands of dollars over the life of your loan. Timing is another critical element. Mortgage rates today fluctuate daily based on economic data, bond market performance, and Federal Reserve policies. Monitoring these trends can help you identify favorable conditions for locking in a rate. For example, if you notice that rates have dropped due to a weaker-than-expected jobs report, it might be an opportune moment to act. Many lenders offer rate-lock options, allowing you to secure a specific rate for a set period while you finalize your home purchase. This can protect you from potential rate increases during the loan processing period.

Read also:

What Steps Should You Take to Compare Mortgage Rates Today?

Comparing mortgage rates today is essential to ensure you're getting the best deal. Start by obtaining quotes from multiple lenders, including banks, credit unions, and online mortgage platforms. Pay attention not only to the interest rate but also to additional costs, such as origination fees, closing costs, and discount points. These factors can significantly impact the overall cost of your loan. Additionally, consider the type of loan that best suits your needs—whether it's a fixed-rate mortgage for long-term stability or an adjustable-rate mortgage for short-term savings.

How Can a Mortgage Broker Help You Find the Best Rates Today?

Working with a mortgage broker can simplify the process of finding the best mortgage rates today. Brokers have access to a wide network of lenders and can negotiate on your behalf to secure competitive rates. They can also guide you through the complexities of loan terms and conditions, ensuring you fully understand the implications of your choices. While brokers charge fees for their services, the potential savings they deliver often outweigh the costs, making them a valuable resource in your homebuying journey.

Is Now the Right Time to Buy with Mortgage Rates Today?

Deciding whether now is the right time to buy a home hinges on several factors, including mortgage rates today, personal financial readiness, and broader market conditions. While mortgage rates today are a critical consideration, they shouldn’t be the sole determinant of your decision. For instance, if you’ve been saving for a down payment, have a stable income, and are ready to settle into a long-term residence, a favorable rate environment can make buying more appealing. On the other hand, if you’re financially unprepared or uncertain about your long-term plans, waiting might be the wiser choice, even if mortgage rates today seem attractive. Market dynamics also play a role. Historically low mortgage rates today can fuel competition among buyers, driving up home prices and creating a seller’s market. In such conditions, you might find yourself competing with multiple offers or struggling to afford homes within your budget. Conversely, if mortgage rates today are higher, it could deter some buyers, leading to less competition and potentially more negotiating power. Understanding these dynamics can help you assess whether the current market aligns with your goals.

How Do Mortgage Rates Today Compare to Historical Trends?

To gauge whether now is the right time to buy, it’s helpful to compare mortgage rates today with historical averages. Over the past few decades, rates have fluctuated significantly due to economic cycles, inflation, and Federal Reserve policies. For example, during the early 1980s, mortgage rates soared above 18%, while in recent years, they’ve hovered around historic lows, often below 4%. While mortgage rates today might not be at their absolute lowest, they could still be more favorable than long-term averages, making them worth considering if you’re ready to buy.

What Are the Risks of Waiting for Lower Mortgage Rates Today?

Waiting for mortgage rates today to drop further carries its own risks. Economic conditions can change rapidly, and rates might rise unexpectedly due to factors like inflation or Federal Reserve interventions. Additionally, delaying your purchase could mean missing out on homes in your desired area or facing higher home prices in the future. If you’re financially prepared and confident in your decision, acting now could save you from potential regrets down the line. However, if you’re unsure